A Whole New Way of Thinking about - Funding Pension & OPEB Benefits

When was the last time your benefits consulting firm assembled a room full of attorneys, actuaries, accountants, bankers, insurance and benefits professionals to find the BEST solution for your Underfunded Pension and OPEB issues?

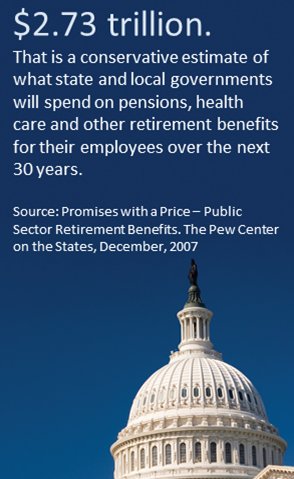

Pay-as-you-go, got up and went, courtesy of the Financial Accounting Standards Board (FASB) and Governmental Accounting Standards Board’s (GASB) issuance of accounting standards over the past 20 years. Now both public and private employers that provide post-retirement benefits must actuarially determine the amount of their future liability. These accounting rules apply to pensions as well as Other Post Employment Benefits (OPEB), primarily retiree health benefits. While these accounting rules do not mandate the funding of the future liability, they do require that the liability be accounted for in financial statements.

The true impact of these accounting standards is not the amount of the liability for retiree benefits – the number and liability have always existed.What has changed is that the amounts are now known to the public. The amount of these liabilities is now known by employees, unions, creditors, voters, and most importantly bond and credit rating agencies. Having received the mandated actuarial valuation the employer's financial liability is quantified and the question becomes - “What do we do now?”

While many of the major actuarial and benefits consulting firms have risen to the occasion of providing the needed actuarial valuations, they have failed to provide more than a cookie-cutter approach for resolving the issue of unfunded liabilities. In 2008, we brought together under one roof a multidisciplinary team for a three-day Solutions Summit. These professionals had one goal in mind – adapt the benefits and financing models that have worked for decades in the private sector for use in the public sector. Each member of the team cut their teeth in designing and financing benefit plans and have redeployed these innovative strategies to solve the funding issues for public and private sector pension and OPEB liabilities

The ARC TrustTM

We have developed The ARC TrustTM utilizing an approach designed for private industry. The ARC TrustTM has been specifically tailored to allow governments and private sector employers of all sizes to fully fund pension and retiree health care benefits. Utilizing an economic and actuarial funding model, The ARC TrustTM can provide for the full funding of retiree benefits in a manner which will satisfy an employer's GASB and FASB reporting and disclosure requirements. Imagine, the ability to continue to recruit, reward and motivate workers with:

No Increase in Debt • No Increase in Vesting • No Reduction in Retiree Benefits

"Innovation by definition will not be accepted at first. It takes repeated attempts, endless demonstrations, monotonous rehearsals before innovation can be accepted and internalized by an organization. This requires “courageous patience”

Warren Bennis